DARKHORSE--from tech to market, for the long run.

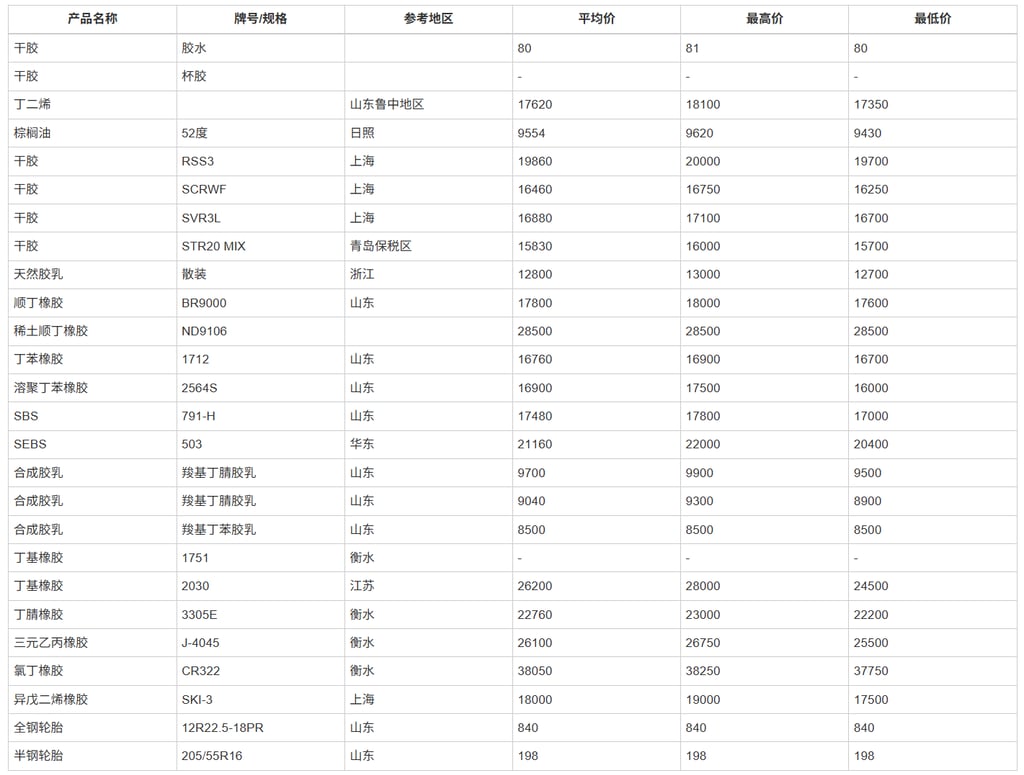

2026 week 14 material price in China

for rubber and tire industry

DH MKT TEAM

4/6/20262 min read

Week 14 Price Commentary

Week 14 marked a clear, broad-based upward shift across the rubber and elastomer market, with prices rising across most product categories despite a decline in upstream butadiene. The market is evidently pricing in geopolitical risk rather than spot feedstock cost.

Upstream Feedstock

Butadiene (Shandong) fell from RMB 18,140/mt (Week 13) to RMB 17,620/mt (Week 14), making it the only major upstream material showing a clear decline.

This weakness, however, failed to transmit downstream, indicating a decoupling between feedstock cost and elastomer pricing.

Natural Rubber

All major grades recorded synchronous increases:

RSS3 (Shanghai): 19,640 → 19,860

SCRWF (Shanghai): 16,210 → 16,460

SVR3L (Shanghai): 16,660 → 16,880

STR20 MIX (Qingdao bonded): 15,482 → 15,830

Natural latex (Zhejiang): 12,510 → 12,800

This confirms a systemic upward repricing, rather than isolated spot movements.

Synthetic Rubber

Synthetic rubber prices strengthened across the board, despite lower butadiene:

BR9000: 17,590 → 17,800

Nd-BR (ND9106): 27,500 → 28,500

SBR 1712: 16,300 → 16,760

SSBR 2564S: 15,460 → 16,900

SBS 791-H: 16,320 → 17,480

SEBS 503: 19,280 → 21,160

IIR 2030:23,250→26,200

This reflects forward-looking risk pricing, driven by energy and supply concerns rather than immediate cost input.

Downstream Tires

All-steel and semi-steel tire prices remained unchanged week on week.

A clear cost-price scissors gap is forming, with margin pressure accumulating downstream.

In Week 14, butadiene prices edged slightly lower, mainly reflecting a correction of earlier panic-driven sentiment, rather than any meaningful improvement in fundamentals. In contrast, most major rubber products recorded higher transaction average prices, including natural rubber (NR) and synthetic rubbers, confirming a clear divergence between upstream feedstock movement and downstream elastomer pricing.

Overall, price increases were broad-based, with certain products showing particularly strong gains. Butyl rubber stood out, posting an increase of around RMB 3,000/mt (more than USD 400/mt) week on week, highlighting the market’s heightened sensitivity to supply-side risks.

These price dynamics reflect growing market concern that the Iran-related geopolitical situation is unlikely to be resolved in the short term. This concern is further amplified by production disruptions, including the shutdown of Sibur facilities, which has tightened supply expectations across several elastomer segments.

As a result, the market is now experiencing a structural supply–demand imbalance, where risk premiums are being rapidly repriced despite limited changes in immediate consumption. In the short term, this imbalance is likely to intensify further toward late April, particularly if geopolitical tensions persist and supply-side constraints remain unresolved.