DARKHORSE--from tech to market, for the long run.

2026 WEEK 12 MATERIAL PRICE IN CHINA

For rubber and tire industry

DH MKT TEAM

3/23/20262 min read

I. Overall Market Overview

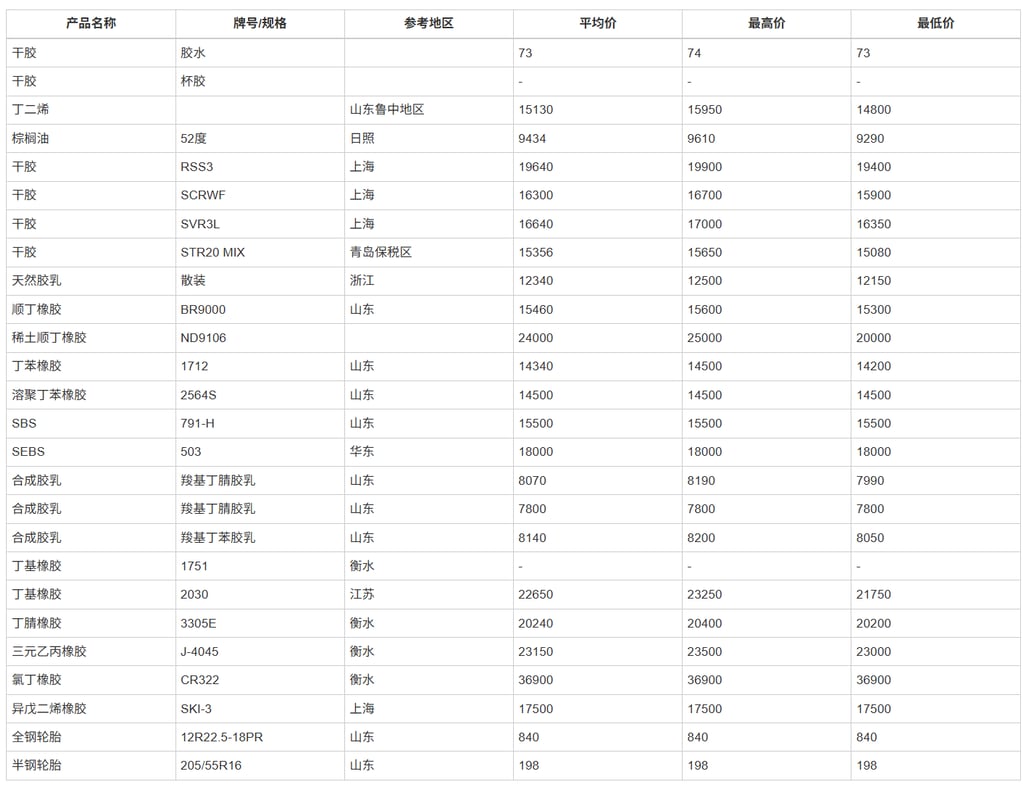

The Iran conflict has entered its third week. Shipping through the Strait of Hormuz remains severely disrupted, with approximately 20% of global oil supply still offline. Brent crude continues to trade at elevated levels (cumulative gain >50%). Petrochemical cost transmission has accelerated, driving broad-based increases in synthetic rubber prices, while natural rubber showed a temporary pullback this week, further widening the polarization between natural and synthetic segments.

Ⅱ.Core Market Commentary

Synthetic rubber sees broad-based sharp increases – cost-driven rally

The oil/petrochemical shock from the Iran situation has deeply penetrated the synthetic rubber chain. Butyl rubber (+1,300 yuan/ton), SSBR, EPDM and other high-value grades recorded significant gains. Some scarce grades (e.g. rare-earth BR ND9106) even spiked to 24,000 yuan/ton, reflecting strong market anticipation of medium-to-long-term supply tightness.Natural rubber corrects temporarily but retains relative resilience

Mainstream dry natural rubber grades fell 400–550 yuan/ton this week, mainly due to inventory buildup at Chinese ports and the gradual start of the tapping season in Southeast Asia. However, with crude remaining elevated, the cost-competitiveness advantage of natural rubber versus synthetics continues to widen; a high-oscillation, firm bias is likely to persist.Price spread keeps expanding – tire industry cost pressure intensifies

The gap between natural and key synthetic grades (especially butyl, nitrile, EPDM) has widened further. Raw material procurement costs for downstream tire, hose, seal and other manufacturers have risen markedly. While all-steel and PCR tire prices held steady this week, multiple producers have already indicated plans to implement fresh price increases next week or later in the month.

Ⅲ. Near-term Outlook & Recommendations

Closely monitor progress on Strait of Hormuz reopening and the latest military/political developments involving Iran, Israel, and the United States. Any meaningful de-escalation signal could trigger a short-term correction in crude and synthetic rubber.

Should the conflict persist (beyond 4–6 weeks), synthetic rubber supply tightness will likely become entrenched, with butyl, EPDM and other premium grades retaining upside potential.

Suggestions for downstream players:

Consider locking in select synthetic rubber long-term volumes ahead of further rises;

Optimize compound formulations by increasing the proportion of natural rubber where technically feasible;

Carefully manage finished goods inventory and pricing cadence to avoid margin squeeze.

(Data sourced from weekly market quotations; actual transactions shall prevail)